LOW BTU AFL

LOW

LOW share count

12/31/99: 1.52 billion

6/30/25: 560.44 million

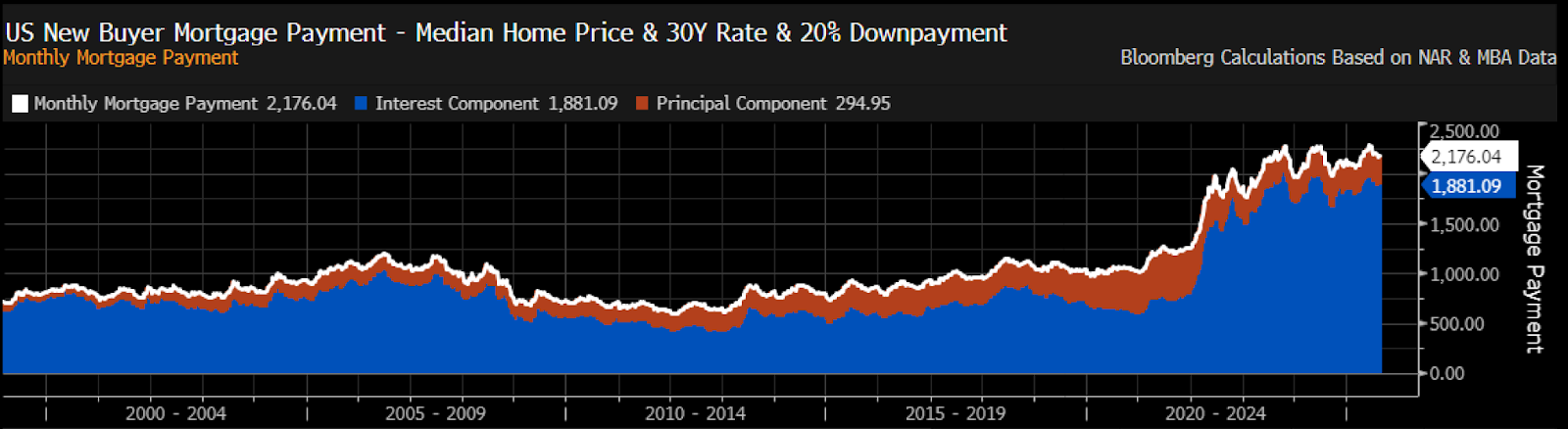

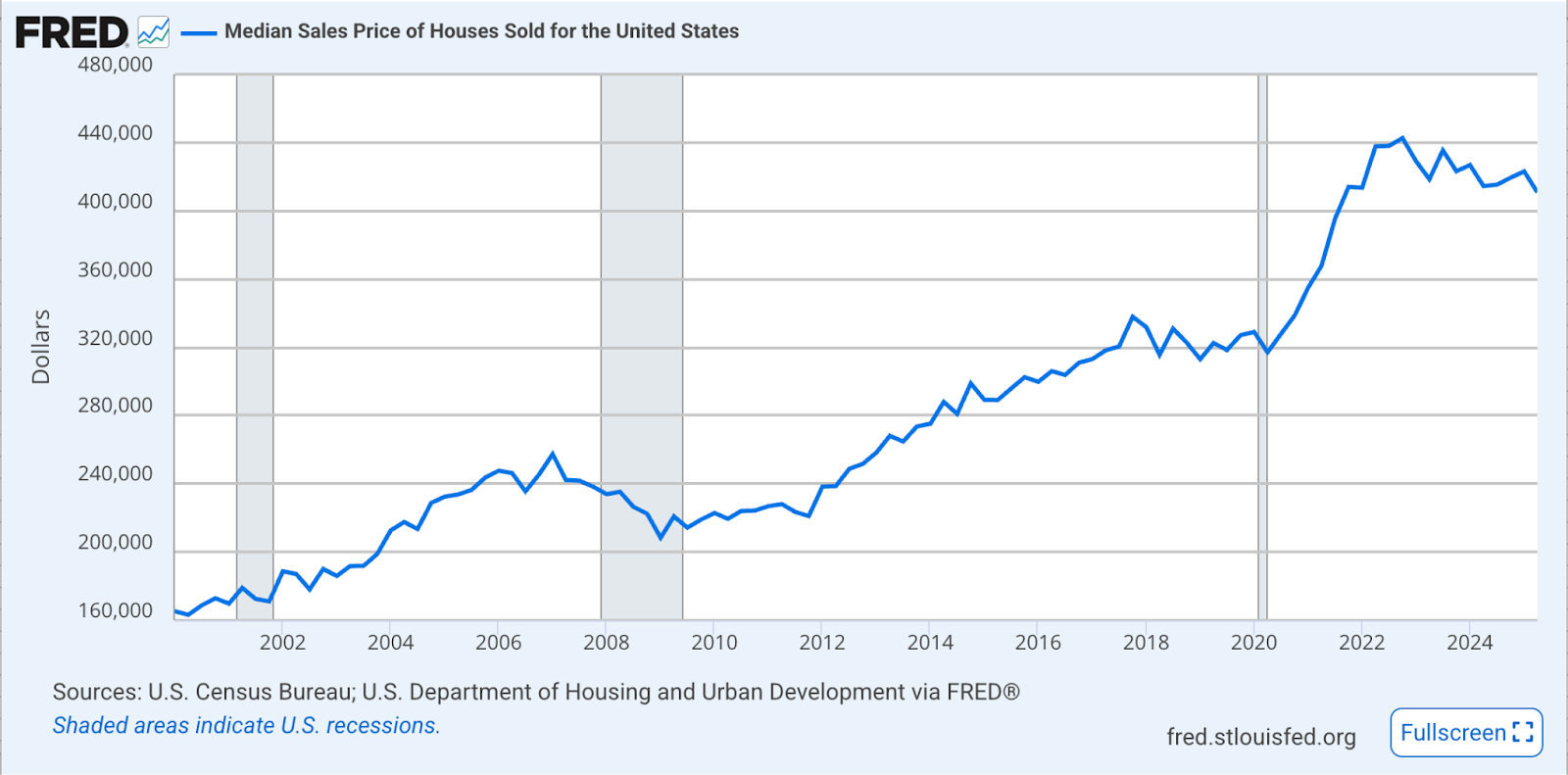

Bye-bye to LOW’s buyback engine until Q2 2027 and hello recession in Q4 2025. Just kidding. However, LOW’s words and actions are awfully pessimistic. They’re paying down debt for the near future to remain investment grade, citing a depressed housing market, and are guiding to flat or 1% revenue growth. All of that was trounced by their last hoo-rah acquisition of Foundation Building Materials for $8.8 billion. LOW finished the week in the green by four odd percent.

“Pascal said that the heart has its reasons that the reason doesn’t understand. For ‘heart’ read ‘Wall Street’”. — Benjamin Graham

BTU

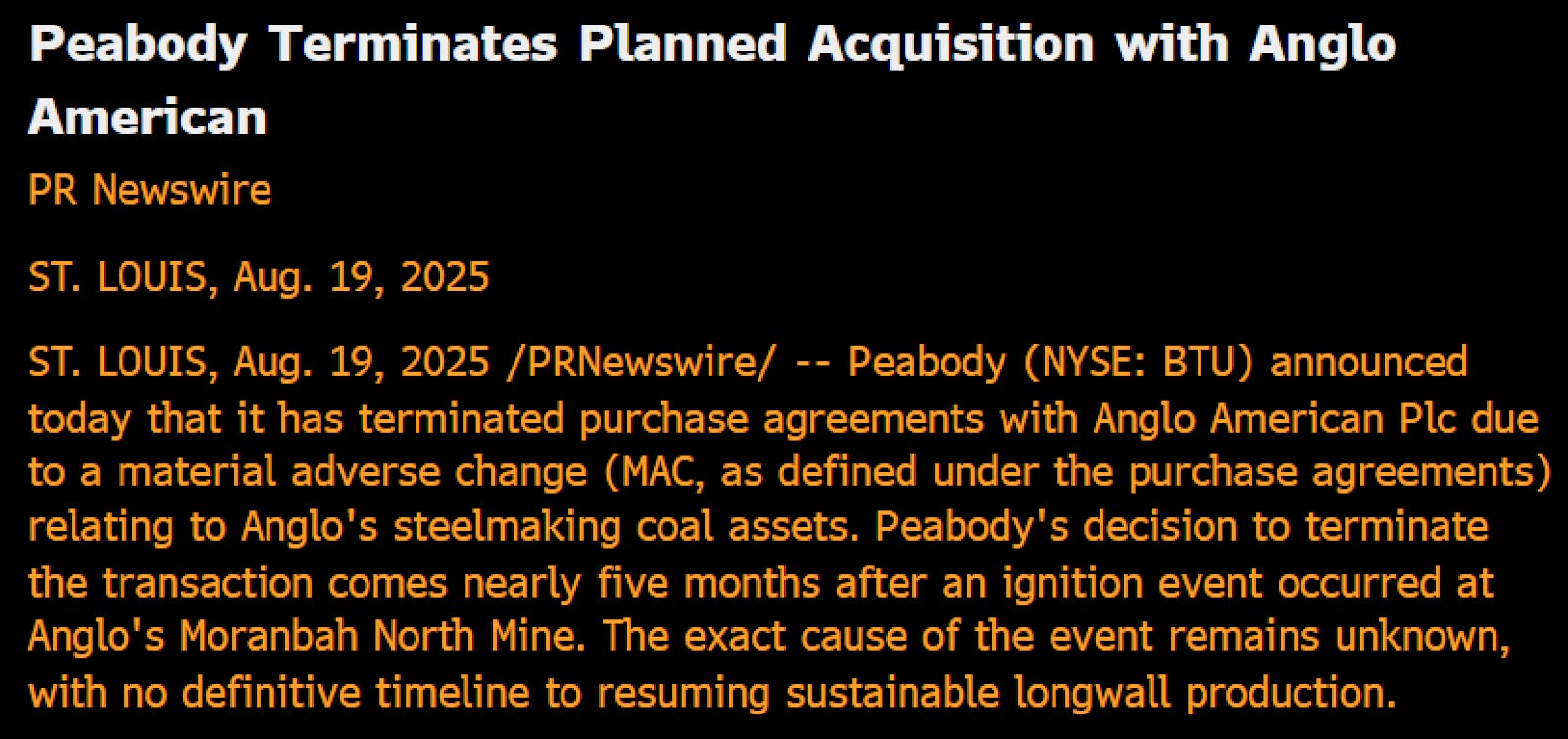

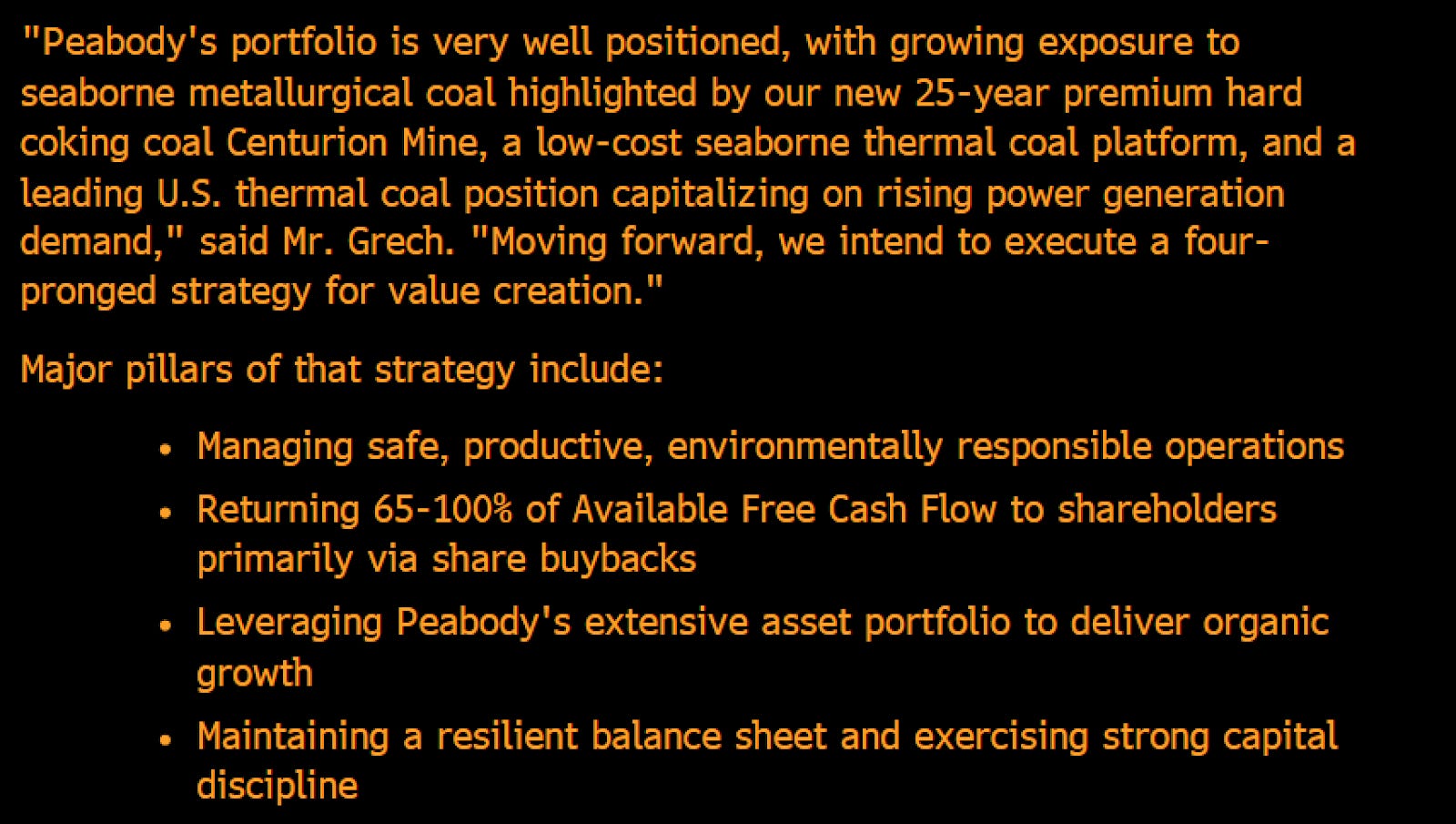

9.7 billion tons of coal were consumed globally last year and Peabody (BTU) supplied about 1.23% of that, or 120 million tons. Now that’s a shadow of China’s Shenhua Energy, which cranked out around five billion tons, yet BTU is the largest coal producer in the United States. Before pulling out, BTU was set to be $3.8 billion larger by acquiring Anglo American met coal assets. BTU got wet feet, however, because of a fire at Anglo’s Moranbah North Mine that happened five months ago. In BTU’s eyes, there was a material adverse change or “MAC” to the assets. Of course, Anglo is pissed. Though BTU shareholders should be jumping for joy. Management expressed their love for BTU’s assets and will use 65% to 100% of free cash flow to repurchase shares — quite a reassuring pivot. In 2016, coal prices plunged, and BTU went bankrupt due to its abuse of debt-fueled acquisitions.

The stock popped 60% or so off its April lows and currently trades at an EV/FCF of 8.32x. In Q2, Gate City purchased 644,221 shares.

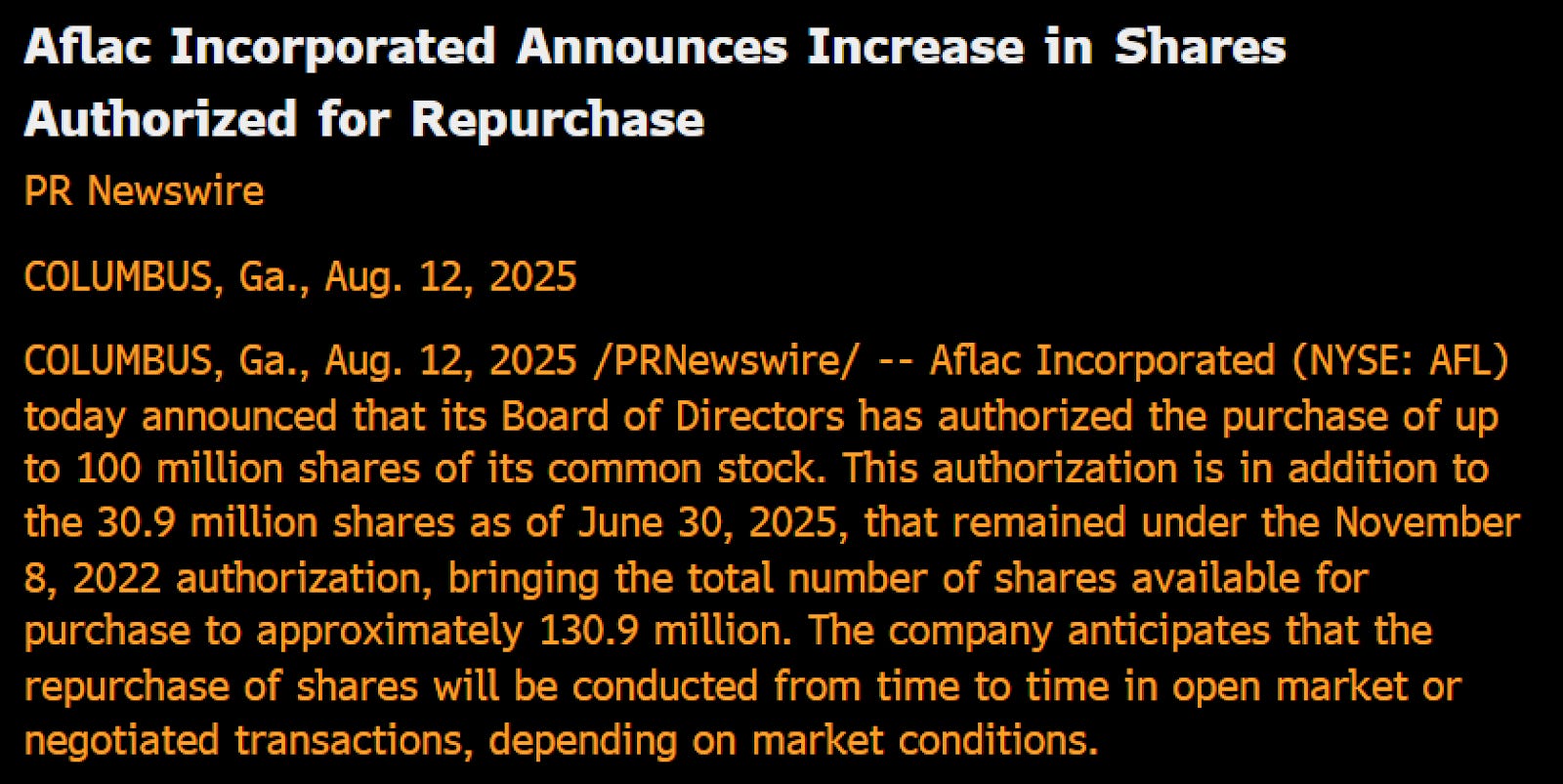

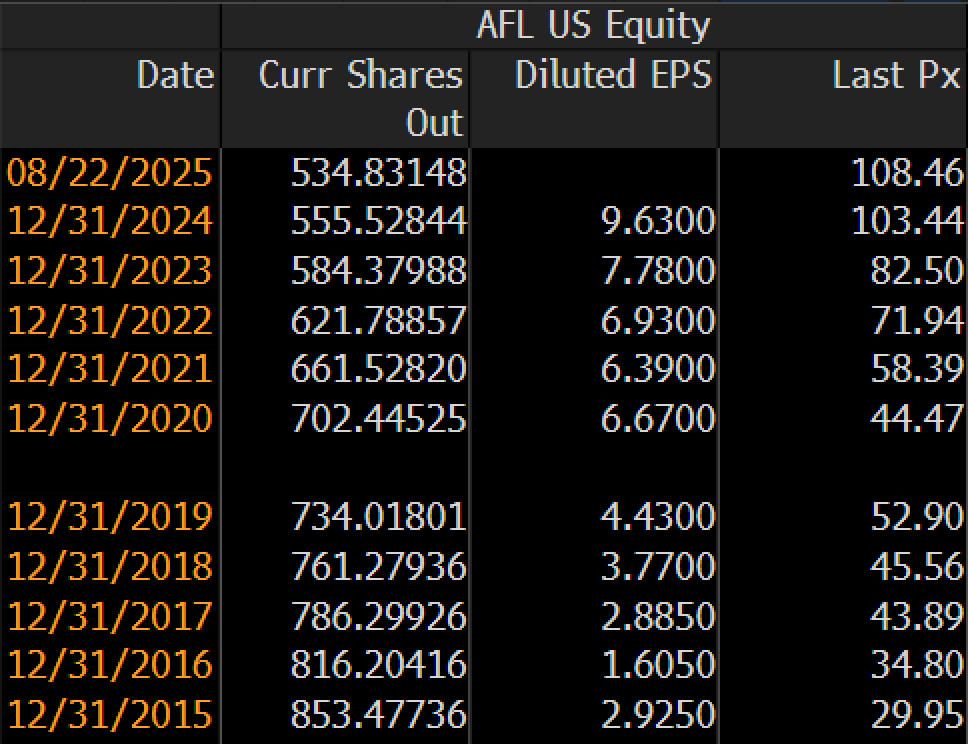

AFL

Authorized buybacks now amount to nearly a quarter of shares outstanding.

AFL provides supplemental insurance to individuals in the United States and Japan. Products include accident and disability, cancer expense, short-term disability, sickness and hospital indemnity, hospital intensive care, and fixed-benefit dental plans. 50% of AFL’s revenue is generated from Japan, where they have 114,000 licensed sales associates. AFL also has agreements with approximately 90% of banks in Japan to sell its products. Advertising spend over the last three years was $181 million, $188 million, and $204 million, respectively. From the numbers below, Nick Saban, Deion Sanders, and that duck seem to be worth every penny.

The past decade saw returns on equity over 15%, a share count that dwindled 37.3%, a 229.8% boom to EPS, and a three-bagged stock. It’s been great to own AFL, but surprisingly, the stock isn’t popular, even amongst the quality compounder crowd. VIC has zero write-ups, and there’s limited conversation on X. Probably because the stock trades so smoothly, that is, when the world is bliss. AFL fell three quarters during the GFC and gapped down a half when the pandemic hit. It trades at 2.18x book value right now. A stock for the watchlist, and I’d think it’s on BRK’s too. Insurance, Japan, the duck, the gecko, float, a $58.01 billion market cap. Cut that in half, and it’s still a decent needle mover.

Another banger from Waterboy !!