June 8th-12th

MOS, BRBR, JCTC, CVR, SGA, SKAS, EDUC, NUS

Mosaic (MOS) — “Raw material prices are at unsustainable levels, and they will come down once global trade flows resume. More importantly, the long-term phosphate supply and demand picture has not changed. Phosphate supply is very tight now and will remain tight when more normal economic conditions resume. We've built Mosaic to be resilient, and we're demonstrating that resilience now.” — CEO Bruce Brodine (Q1 2026 earnings call)

The Strait of Hormuz blockade has sent sulfur and ammonia prices soaring. Mosaic’s margins have been squeezed, and earnings per share have collapsed 89.8% from $0.49 in Q1 2025 to $0.05 in Q1 2026 (non-GAAP).

Mosaic has slashed its 2026 capital expenditure guidance by $250 million, implemented production curtailments at several facilities, and targeted $150 million in operational savings to protect cash flow through the end of the year.

Historically, it has paid off to buy shares of MOS when it is trading well below book value. However, the Strait of Hormuz has never been shut down, and it is wishful thinking to believe normal economic conditions will resume with speed. The uncertainty around near-term fundamentals is creating the opportunity, and the worse it gets, the better.

Bellring Brands (BRBR) — Stock is down 88.8% from its 2025 high. Market cap $1.04 billion at $8.91/share (116.28M shares). EV $2.3 billion. TTM revenue $2.3 billion, net income $158 million. Trailing P/E 6.6x, P/S 0.4x. EV/EBIT 6.3x. Long-term debt $1.2 billion. Cash of $33 million. EBIT/interest expense 4.9x.

Share repurchases totaled $486.4 million last year, nearly half of the current market. They repurchased another $26 million in Q2. “As of March 31, 2026, BellRing had $516.9 million remaining under its share repurchase authorization.”

Founded in 2019 (spun out of Post Holdings). American consumer packaged goods company in the convenient nutrition/protein category. Key brands: Premier Protein (leading RTD shakes), Dymatize (protein powders), and PowerBar.

Customers are not happy with the formula change. They are also dealing with a flood of competitors.

Jewett Cameron (JCTC) — 13D filing last month -- Bradley family (Adam Bradley, Melinda Bradley, AJB Investment Fund II, LP, and AJB Capital, LLC) collectively owns 287,066 shares (8.2% of the company).

Market cap $6.4 million at $1.83/share (3.52M shares outstanding). EV $10.2 million. Book value per share $4.43 (P/B 0.42x). TTM revenue $42.2 million, net income -$8.1 million (EPS -$2.30), bank indebtedness of $4.3 million, cash of $0.55 million.

Terry Schumacher, former CFO (’07-’09) of Jewett-Cameron, arrives at a $ 7.00-per-share liquidation value. He writes about the company on Substack —

The company was founded in 1953. Headquartered in North Plains, Oregon. They manufacture and distribute pet, fencing, and other specialty products.

Chicago Rivet & Machine (CVR) — Market cap $9.7 million at $10.00/share (966k shares outstanding). TBV per share $19.09 (P/TBV 0.52x). 2025 revenue $27.9 million, net income -$1.1 million, no long-term debt, cash $1.45 million. Has paid a small dividend (recently temporarily suspended). Auditors issued a “going concern” qualification in May 2026.

Founded in 1920. Illinois-based (Warrenville) manufacturer of cold-formed rivets, fasteners, and screw machine products. John Morrissey and the estate of Walter Morrissey collectively own 18.1% of the company.

** Stanley Kesselman owns 4.1% of the shares outstanding. He also owns 6.2% of Saga Communications.

Saga Communications (SGA) is now trading at $8.91 with a GAAP book value of $23.30, so P/B of 0.38x. Conservatively, book value is probably around $15. Market cap is $56.6 million. Enterprise value is $31.2 million. Cash of $30.4 million and long-term debt of $5 million.

In 2022, Gate City was buying shares at $20 and had a fair value of $30. They about doubled their position in Q4 2024, haven’t sold a single share since, and currently own 13.6% of the company.

This could be a good “coattail riding” opportunity. Buffett coined this term in his 1962 partnership letter —

“Many times generals represent a form of ‘coattail riding’ where we feel the dominating stockholder group has plans for the conversion of unprofitable or under-utilized assets to a better use. We have done that ourselves in Sanborn and Dempster, but everything else equal we would rather let others do the work. Obviously, not only do the values have to be ample in a case like this, but we also have to be careful whose coat we are holding.”

Gate City has been constructive with Saga, writing them a long email in March 2025: https://sec.gov/Archives/edgar/data/886136/000139834425006054/fp0092831-1_ex99e.htm

They want Saga to stop wasting money and management time on digital ads, sell the “Saga House” which is a luxury Florida beach residence, fix compensation, and get back to running a tight, profitable radio company while returning cash to owners.

While they’ve yet to sell the Saga House or ditch the digital ad business, they did sell 22 tower sites for $10.7 million in Oct 2025 and repurchased 2.8% of shares outstanding in a single privately negotiated transaction announced on Dec 15, 2025.

Gate City, as a 13.6% shareholder, reduces the risk of management impairing intrinsic value to a significant degree. This fact, paired with a cheap price, provides a nice margin of safety.

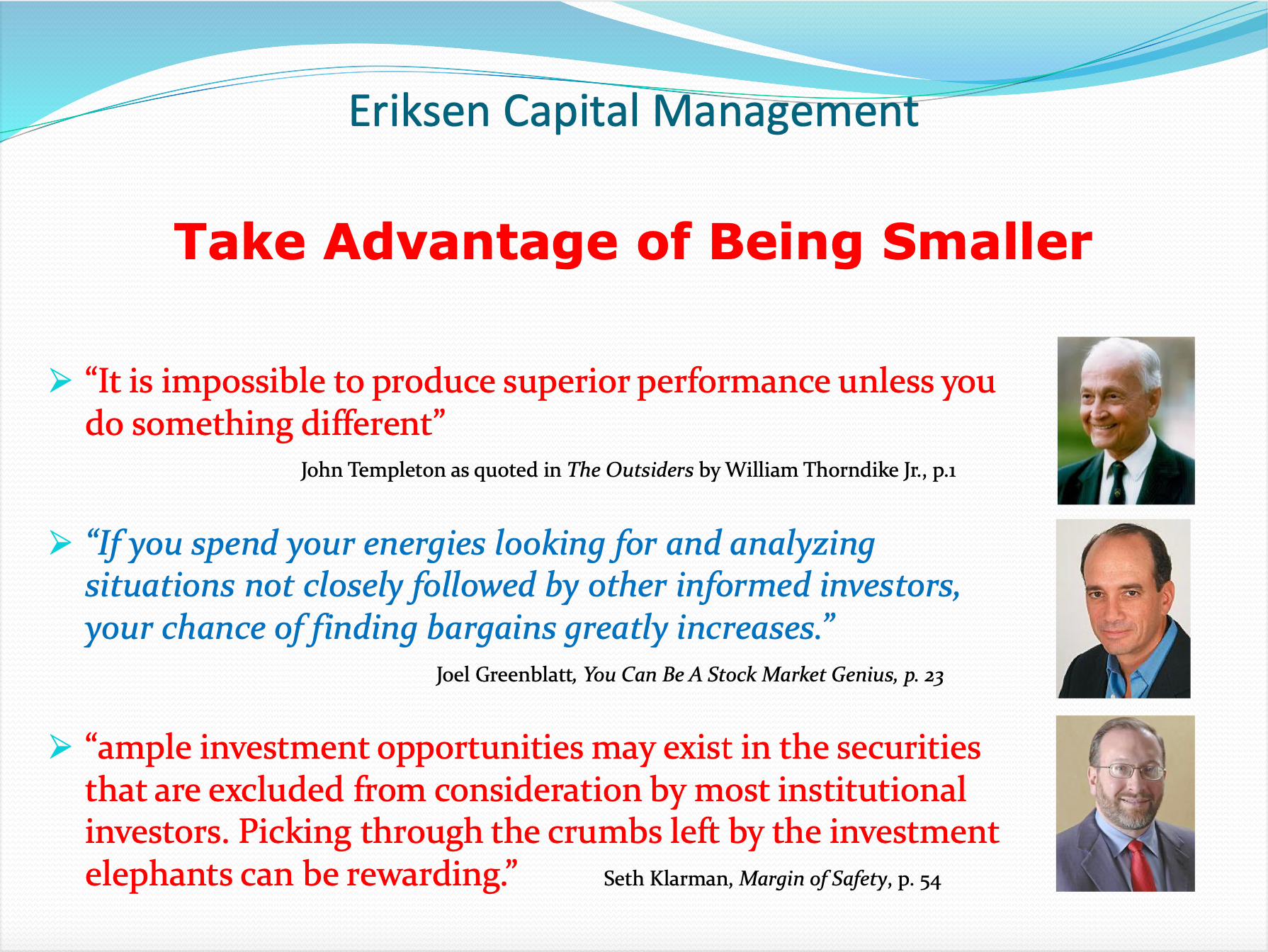

Tim Eriksen (Eriksen Capital Management) has an amazing track record investing in very small stocks.

From his fund presentation (Jan 2026):

Educational Development Corp (EDUC) — Owner and exclusive publisher of Kane Miller children’s books, maker of toys (Learning Wrap-Ups and SmartLab), and exclusive distributor of Usborne children’s books. Insiders own 25% of the company.

Market cap of $11.6M at $1.36/share and EV of $17.2 mil (all debt is operating leases). Tangible book value per share is $5.03 -- P/B 0.27x, P/S of 0.51x on FY2026 revenue of $22.9 mil. Sold Hilti HQ/warehouse for $32.2M (Oct 2025), repaid $31M bank debt, now leasing back.

Management reduced inventory levels from $44.7 million to $37.7 million, generating $7 million in cash flow. Corporate restructuring involving executive pay cuts and staff reductions is expected to save over $1.2 million in annual expenses starting in fiscal 2027.

NU Skin Enterprises (NUS) — Market cap of $264 mil. at $5.44/share (48.55M shares). EV is $341 mil. Book value per share $16.34 (P/B 0.33x); TBV per share is $13.82. TTM revenue $1.4 bil, net income $54.5 mil (EPS $1.08), trailing P/E 5.0x, P/S 0.19x. Long-term debt of $203.6 mil, which is down from $478 mil in 2023. Cash of $200 mil. Dividend yield is 4.4%.

Founded in 1984. American multi-level marketing company offering beauty, personal care, and wellness products globally. Sold Mavely affiliate platform in 2025 for about $250M and is using proceeds for debt reduction, innovation, and shareholder returns.