HP

Tech outlet “SemiAccurate” reported yesterday that “Nvidia is looking to make a huge purchase that will reshape the PC and server landscape like nothing else has done since the computer was invented. And let us say again, we are dead serious here.”

HP and Dell jumped 5.3% and 6.7% on the news. NVIDIA issued a statement clarifying that the media report was false and that they are not engaged in any discussions to acquire a PC maker.

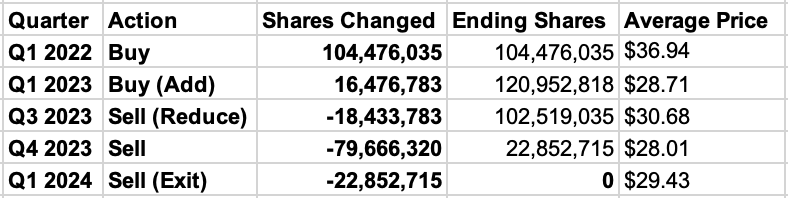

Berkshire got in and out of HP a few years back, owning around 12% of the company at one point. Historical transactions:

Barron’s believed Buffett was behind the buying.

“Why? Combs and Weschler run pension-fund investments for Berkshire, and none of its pension funds hold HP stock. Based on this pension-fund indicator, Berkshire holdings DaVita (DVA), Kroger (KR), Ally Financial (ALLY), Louisiana-Pacific (LPX), and RH (RH) likely were made by Combs and Weschler. Some large Berkshire equity holdings associated with Buffett, including Occidental Petroleum (OXY) and Chevron (CVX), aren’t held by any pension funds run by Berkshire.”

“For HP, there are no pension-fund holders at Berkshire. Other reasons for suspecting the HP holding was Buffett's was its large initial size, which was more than 10% of the total money run by Combs and Weschler.”

HP was founded in 1939. They’ve paid a dividend since 1965 and have increased it consecutively for the past sixteen years. They basically have no tangible equity in the business and return all free cash flow to shareholders.

CFO Karen Parkhill during HP’s Q1 earnings call on Feb 24th:

“So we do remain committed to returning 100% of our free cash flow to shareholders over time. And we’ve talked about that as long as our gross leverage remains below 2x, and there aren’t higher return opportunities. That said, you’ve seen us be operating with leverage slightly above 2x right now. And we have basically earmarked cash on our balance sheet to repay debt as it comes due in ‘26, and we can continue to do that in ‘27 if needed. All of that combined has enabled us to also return to shareholders. And in Q1, we returned -- we were pleased, honestly, to return about $600 million to shareholders just in our first quarter and over $300 million of that was in share repurchase.

3.4% on your money in Q1 at the current price.

Over the past five years, dividends totaled about $5 billion and share repurchases $13.5 billion. Collectively, that is 105% of HPQ’s $17.6 billion market cap.

“As of January 31, 2026, HP had approximately $8.1 billion remaining under the share repurchase authorization approved by HP’s Board of Directors.”

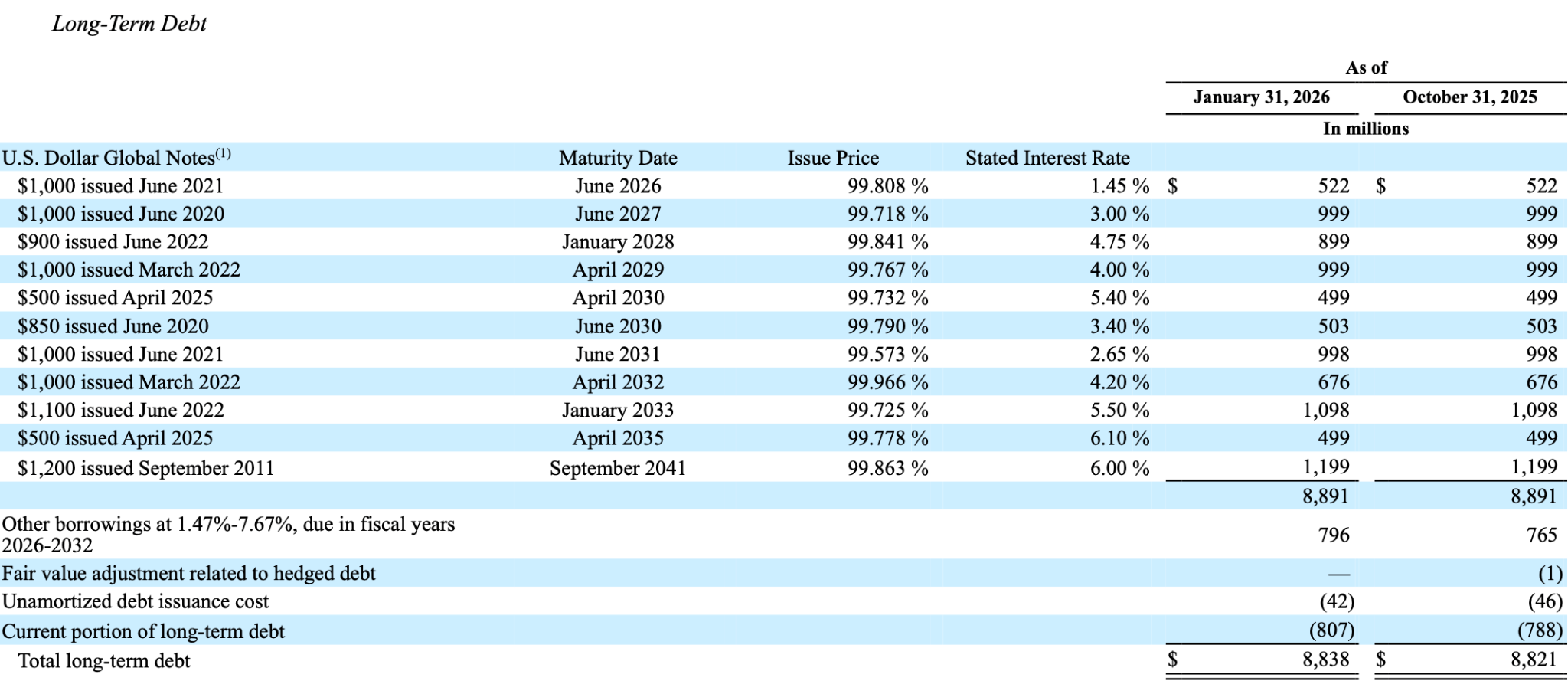

Trailing free cash flow yield is 16.6%. Dividend yield is 6.2%. LTM net debt/EBITDA is 1.62x. Operating earnings to interest expense ratio is about 6x. Cash flow from operations last year was $3.7 billion. Cash on the balance sheet is $3.2 billion. Long-term debt is $8.8 billion and well-laddered.

The stock has been cut in half over the past eighteen months due to the printing business declining and the AI boom driving up chip costs. Memory costs now make up 35% of their PC’s bill of materials, up from 10% only a year ago.

Management has also given cautious guidance. They expect free cash flow to be on the low end of their $2.8 to $3.0 billion range, which is still a 16% yield.

Buffett bought shares at $35 and the stock is now just under $20 — almost 50% cheaper. HP is an interesting, unpopular, large company.

“The large companies thus have a double advantage over the others. First, they have the resources in capital and brain power to carry them through adversity and back to a satisfactory earnings base. Second, the market is likely to respond with reasonable speed to any improvement shown.” — Graham