Cash

“If the market were way overpriced, I wouldn’t own any stocks.” – Walter Schloss

Barron’s - February 25, 1985

Q: Walter, have you ever dabbled in options or anything like that?

A: Never bought an option—well, I can’t say never. I did it once. The market was, I thought, very low, and I bought an index option. I decided I was never going to do it again. I don’t sell short, I don’t do anything with futures—those are all exotic areas that may be good for the brokers: I do not think they’re good for us.

Q: You don’t write options against stocks in your portfolio, either?

A: Right. Because that freezes me. If the market goes up, then I can’t do anything about it. I like maneuverability. And dealing with the options I find a distraction. Life is—you gotta limit yourself a little bit.

“Q: We get the sense that you have a kind of “fair-to-middlin’” view of where the markets going this year… ?

A: I have no opinion on the market. Graham used to have this theory that if there were no working capital stocks around, that meant the market was too high.

Q: Why’s that?

A: Because historically, when there were no working capital stocks, the market collapsed. That worked pretty well till about 1960, when there weren’t any working capital stocks, but the market kept going up. So that theory went out. I simply say, if there are not too many value stocks that I can find, the market isn’t all that cheap. If it were very cheap, there’d be all these stocks floating around. On the other hand, I don’t see the market way overvalued. If the market were way overpriced, I wouldn’t own any stocks.

Q: But you said you’ve never gone to cash.

A: I never have. There’s always a first time. I mean, if the market really went crazy, and you’d say, “Well, I just have to sell, the prices are just out of this world. Xerox is 125. . “ That kind of thing. But I haven’t ever had that position up to now, and I see no reason to think it’ll happen. We just keep on slugging away, trying to find cheap stocks. It’s just a little tougher.”

Schloss kept things simple. No shorting, no options, always staying fully invested in his breed of stocks, that is, until stuff like Xerox trades at 28.4x earnings (Xerox’s EPS was $4.44 in 1985). In that case, sell all of your stocks and call it a day, which Schloss did a decade and a half later after the dot-com bubble bust.

But before liquidating his partnership, Schloss also decided to take advantage of the widespread greed and euphoria, selling short Yahoo and Amazon as they were both valued at well over 100x their revenues.

The trades worked beautifully. Schloss rode off into the sunset, posting returns of 28% and 12% in 2000 and 2001, respectively, versus the S&P’s (9%) and (12%).

I imagine Schloss would be doing something similar today. Maybe shorting stocks like PLTR and CVNA, raising some cash. Or maybe a full flight to cash? “If the market were way overpriced, I would’t own any stocks.”

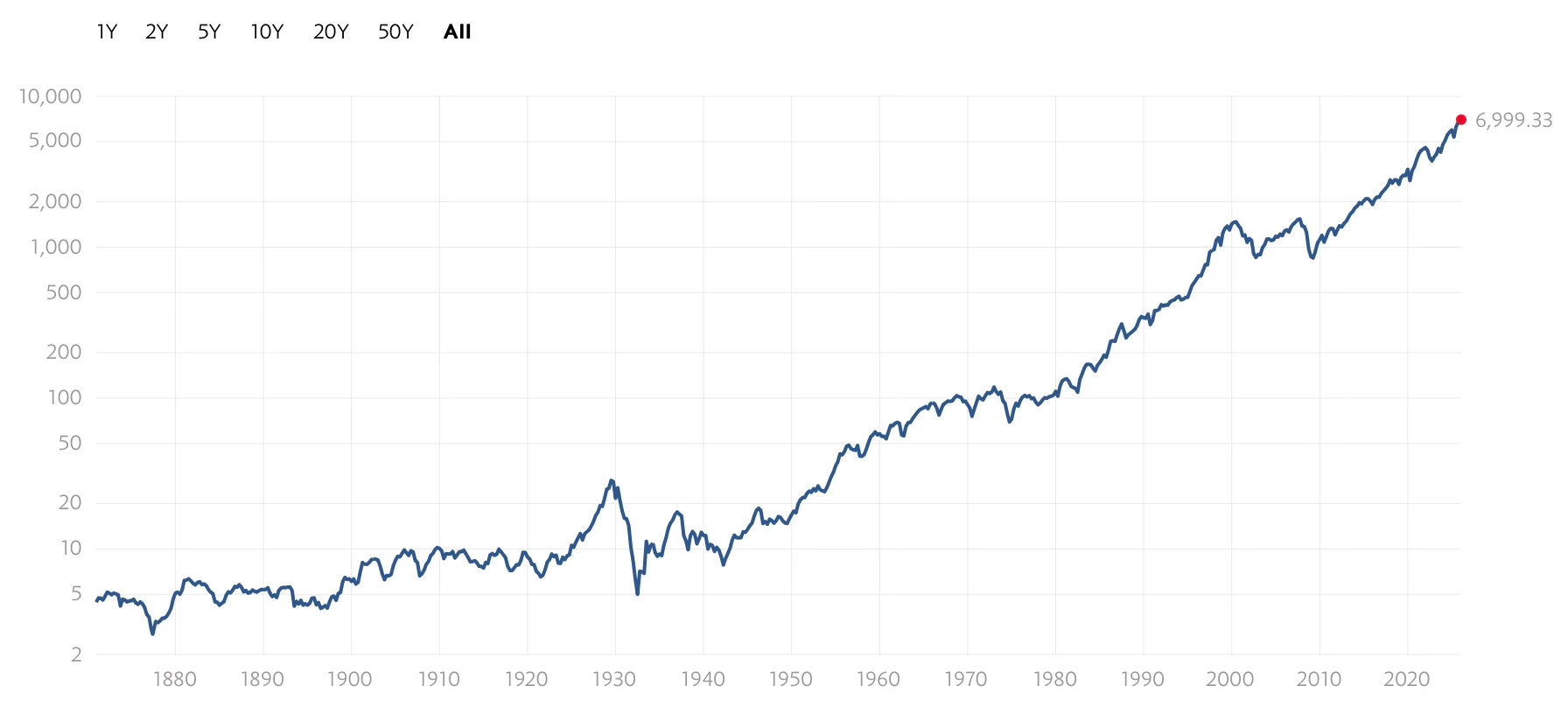

The first time the Shiller ratio ever touched 40 was in December of 1998. It bobbled there until starting its descent in March of 2000 and then finally hit 21 in January of 2003. It sprang to 25 and bobbled there until the GFC hit in September of 2008, collapsing violently to 13.

Seventeen years have passed since the big one and the S&P has only seen two down years, so positive annual returns have occurred 88.2% of the time. 2018 was a soft jab (4.23%) and 2022 was a good blow to the gut (18.04%). Green is all we know.

Yesterday the Shiller closed at 41.02. By all means, the market is way overpriced, and according to Schloss, that means get out of stocks. Why?

“The thing that you would naturally be led into, if you are value-minded, would be the purchase of individual securities that are undervalued at all stages of the security market. That can be done successfully, and should be done -- with one proviso, which is that it is not wise to buy undervalued securities when the general market seems very high.

That is a particularly difficult point to get across: For superficially it would seem that a high market is just the time to buy the undervalued securities, because their undervaluation seems most apparent then. If you could buy Mandel at 13, let us say, with a working capital so much larger when the general market is very high, it seems a better buy than when the general market is average or low.

Peculiarly enough, experience shows that is not true. If the general market is very high and is going to have a serious decline, then your purchase of Mandel at 13 is not going to make you very happy or prosperous for the time being. In all probability the stock will also decline sharply in price in a break.

Don’t forget that if Mandel or some similar company sells at less than your idea of value, it sells so because it is not popular; and it is not going to get more popular during periods when the market as a whole is declining considerably. Its popularity tends to decrease along with the popularity of stocks generally.

QUESTION: Mr. Graham, isn’t there what you might call a negative kind of popularity, such as the variations of Atchison? I mean, in a falling market, while it is perfectly true that an undervalued security will go down, would it go down as fast as some of the blue chips?

MR. GRAHAM: In terms of percentage I would say yes, on the whole. It will go down about as fast, because the undervalued security tends to be a lower-priced security; and the lower-priced securities tend to lose more percentage wise in any important recessions than the higher ones.

Thus you have several technical reasons why it does not become really profitable to buy undervalued securities at statistically high levels of the securities market. If you are pretty sure that the market is too high, it is a better policy to keep your money in cash or Government bonds than it is to put it in bargain stocks.

However, at other times -- and that is most of the time, of course -- the field of undervalued securities is profitable and suitable for analysts’ activities. We are going to talk about that at our next lecture.”