BRK, GOOGL, AAPL

(5/8/17) Buffett: Well, the shares (AAPL), when we bought them at least, were much more reasonable in relation to current earnings. Apple didn’t have to do a lot better in the future than they were doing at the current time. When you get into Google or Amazon, you’re paying for the future more, but then they may well have a better future. I mean that may be more than justified, but, and Apple, I wouldn’t say it’s easier for me to understand than Google now, perhaps or Amazon now, but it certainly would have been five years ago.

It’s amazing where Apple’s ended up with consumers. I mean, I can very easily determine the competitive position of Apple now and who’s trying to chase them, and how easy it is to chase them. We happen to be well situated in terms of having these massive home furnishing stores, and I can learn very easily how consumers react to different things. They’re probably easier than I can trying to pick out what’s really happening at Amazon at any given time.”

(3/31/26) Buffett: “I’m very happy to have it (Apple) be our largest holding. I was not happy to have it be as large as almost everything else combined. Although at a price I was. And it could, it’s not impossible that Apple would get to a price. We would buy a lot of it, but not in this market. I mean, it just isn’t going to happen.”

(5/2/26) Quick: “What is it when you look around, that it’s just prices are too high at this point? I would imagine they are. Greg said this from the stage, too. There are businesses that you like, just not these prices.”

Buffett: “I would say I understand fewer of the businesses as a percentage of whole than I did 10 years ago. I have not learned new industries for some years, so I don’t kid myself on that. I’m not going to learn them. I’m not going to have an edge on, you know, a whole bunch of younger people that have actually grown up with them, used the product, seen things. But, well, as I mentioned, you know, you don’t have to understand too many if they’re like Apple, right?”

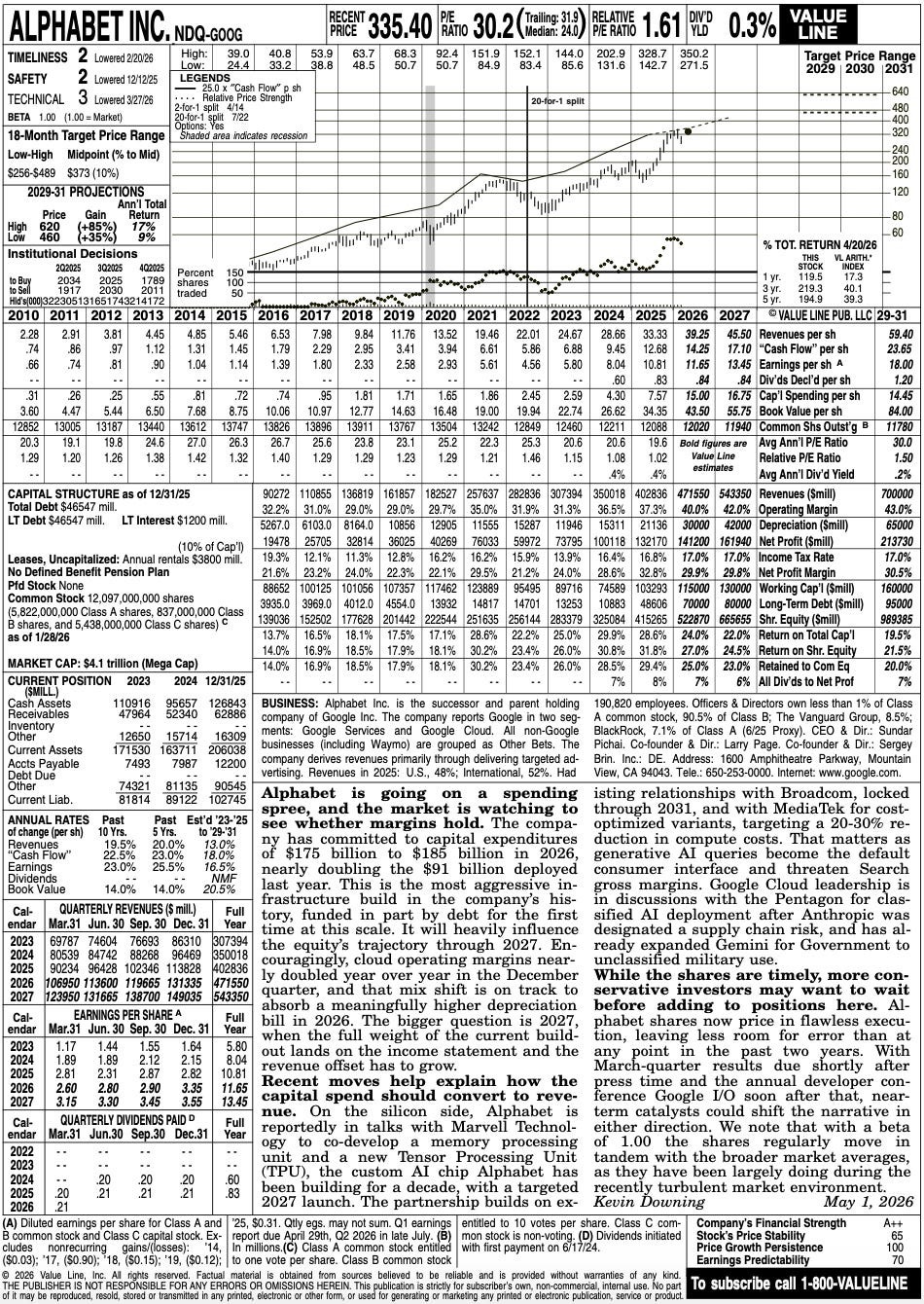

Berkshire purchased $4.3 billion of GOOGL in Q3 2025 and $10 billion in Q1 2026. Their position is currently worth $15.6 billion, about 1.25% of total assets. Here is Google’s most recent page in ValueLine.

Buffett finds Google attractive at 30x earnings. I don’t think he’s ever paid above 20x earnings for anything. He usually pays around 10x pre-tax earnings.

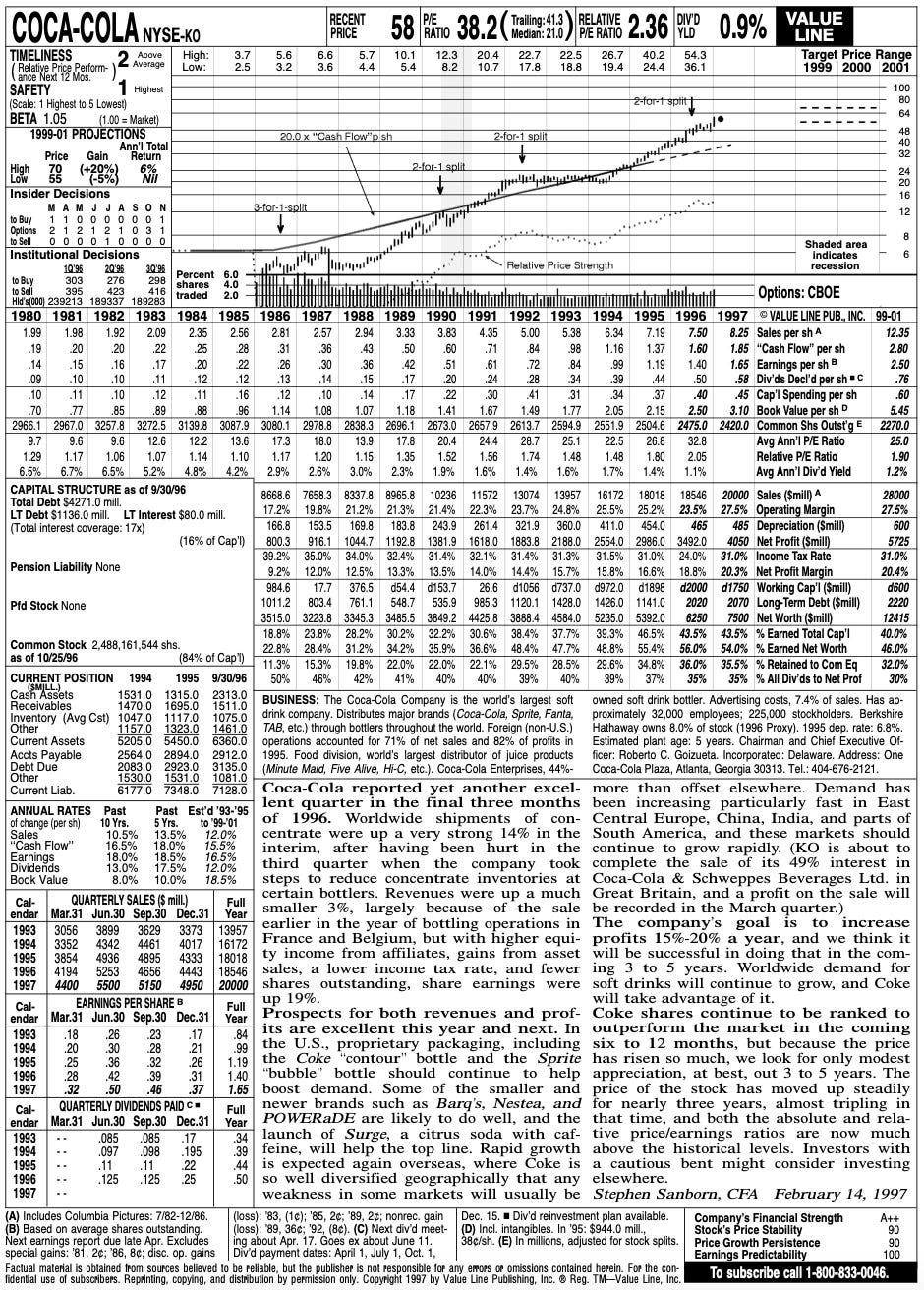

Coca-Cola’s ValueLine page (Feb 1997)

From 1987 to 1997, Coca-Cola’s earnings per share increased 18% and the earnings multiple nearly tripled from 15 to 41, adding 11% to the return. Including the 0.9% dividend yield, KO produced a roughly 30% annualized return for the decade.

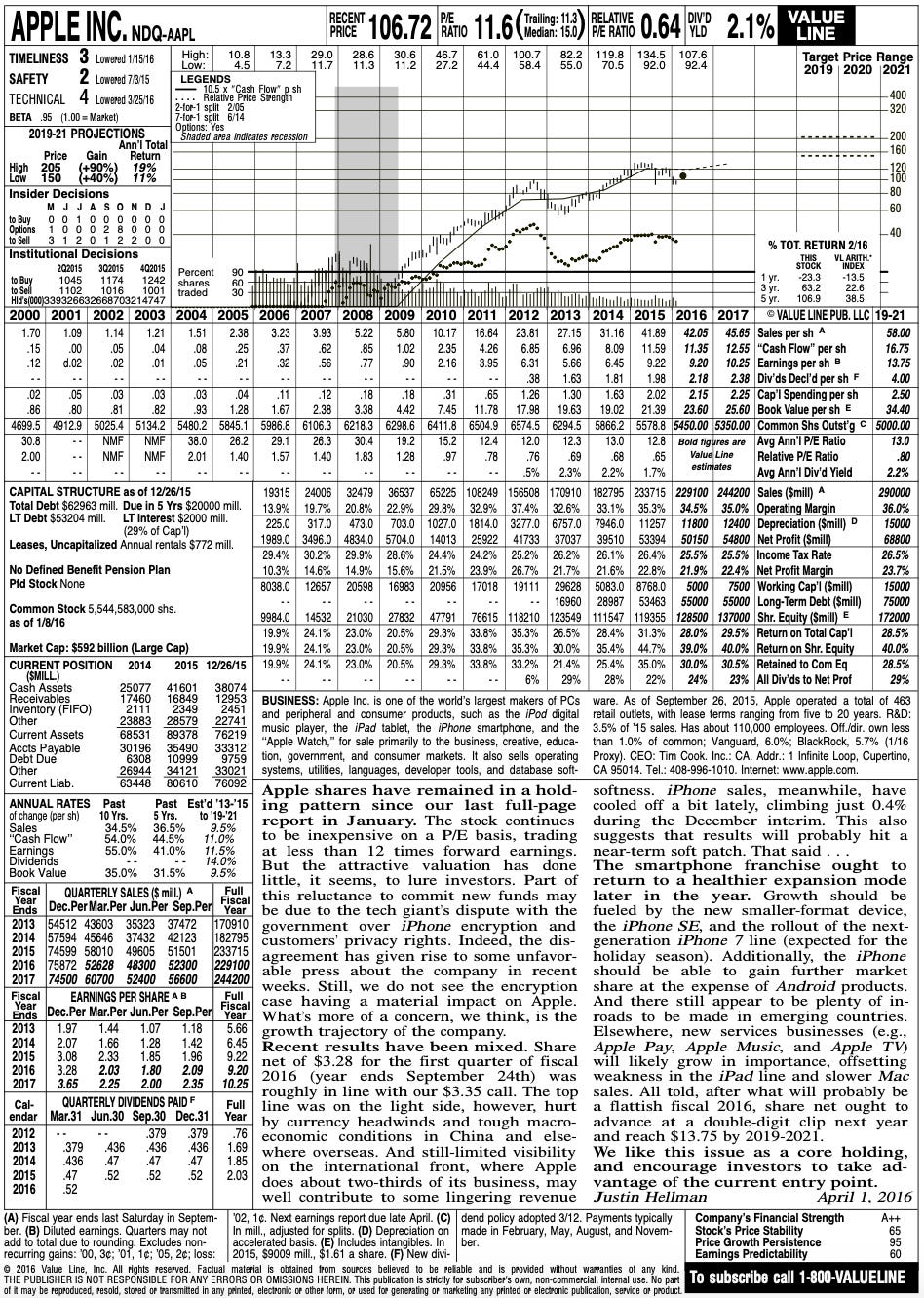

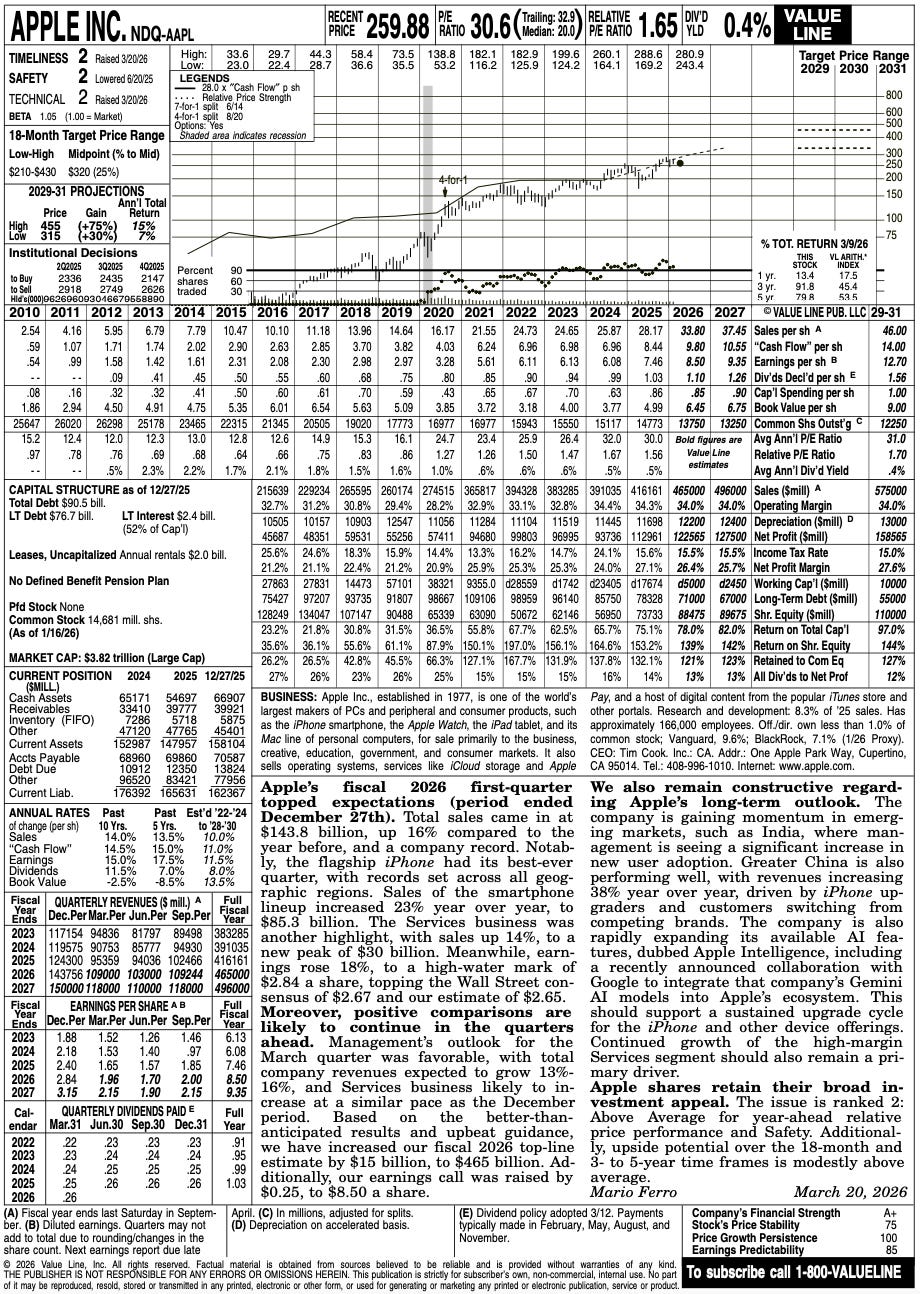

Apple’s ValueLine page (April 2016)

And here’s how the next decade played out.

The dividend yield was 2%, EPS grew 15%, and the earnings multiple approximately tripled from 11.3x to 32.9x for another 11%, so a near 30% annualized return for the decade.

Buffett cut Berkshire’s stake in Apple by 75% over the two and a half years because it got too expensive, trading around 30x earnings. On the other hand, in the heat of a bull market, Berkshire is investing billions into Google, a $4.8 trillion company competing in the AI race that trades around 30x earnings.

Credit Suisse’s “The Base Rate Book” shows that roughly 1/10 companies globally with over $50 billion in sales, from 1950 to 2014, grew earnings at 10-15% over decade-long periods. Google, with $400 billion in sales, is statistically unlikely to compound earnings at a double-digit rate into 2036. Berkshire is betting they will.

Now, if Google does compound earnings at 15% over the next decade and the multiple on 2036 earnings is 15x or 20x instead of 30x, returns would drop to 7.3% and 10.4% annualized, respectively.

I find it very interesting that Buffett, at the annual meeting, said: “It isn’t our ideal surrounding area, or environment, I should say, in terms of deploying cash for Berkshire.”

“Our partial-ownership approach can be continued soundly only as long as portions of attractive businesses can be acquired at attractive prices. We need a moderately-priced stock market to assist us in this endeavor. The market, like the Lord, helps those who help themselves. But, unlike the Lord, the market does not forgive those who know not what they do. For the investor, a too-high purchase price for the stock of an excellent company can undo the effects of a subsequent decade of favorable business developments.” – Buffett (1982 annual report)

It’ll be interesting to see if they allocate more dollars to Google than Apple in the next bear market.

Munger book recommendation: “In the Plex: How Google Thinks, Works, and Shapes Our Lives.”

Buffett on Apple and Google (5/8/17)

Quick: For a guy who claims that he’s not really a technology guy, and in fact doesn’t even own a smartphone, you spent an awful lot of time talking about technology investments that you made or didn’t make, that you missed out on. I was thinking in particular about Apple, you talked quite a bit about why you got into that, IBM why you are selling some of that stake, but you also talked about companies like Google, where you said you missed it and maybe you could tell us a little bit about that.

Buffett: Charlie actually brought up the fact that we missed it too, and Google, I should have had some insight into because GEICO was a heavy user very early on, so here we saw value in something at that time. I have no idea what we’re paying per click now, but we were paying 10 or 11 dollars a click for something that had no cost of goods sold and we were going to keep doing it.

I mean we could see that so I should have had more insight into that. Now whether Bing was going to come along or other people were going to take away the market, that’s another question whether you had sort of a first user advantage that would prevail. And there is a lot of technology to it, so somebody could have come along with a better technological product and I would not have had any insights into that.

I certainly had insights into the benefit to the user, i think blazer surgeon, or something like that, I think it may have sold for 60 or 70 bucks or something of the sort, mesothelioma, I mean that i don’t know what it brings now, but just imagine having something every time you just hit a click you know the cash register rung somewhere out in California.

So it was an extraordinary business and it has some aspects of a natural monopoly. I mean it’s very easy for me when I go to the computer. I’ve worked with Google before, but I’m looking for information for the annual report. I used to have to mail away to federal agencies or go down to the public library and now I can get it in 10 seconds. So it’s a hugely valuable device which the other guy pays for, the user on the computer doesn’t. The answer is we missed it and i knew the fellows they came to see me before they

Quick: Sergei and Larry came to see you?

Buffett: Yeah, and actually Eric did too. Yeah, I liked him.

Quick: So when you say you missed it, that suggests that it’s now at a valuation, you understand the company, but it’s now at a valuation that doesn’t make sense to you. Why don’t you just buy it now?

Buffett: Well, if I was forced to buy it or short it, I’d buy it the same way as Amazon. But it’s a little hard when you look at something at x and it sells at 10x to buy it. It shouldn’t be, but I can just tell you psychologically it’s harder if you looked in the first place and passed at x to then buy it at 10x. That costs people a lot of money in Berkshire. I mean they saw it at a lower price and they just said if it ever gets back there I’ll buy it. That’s a terrible way to think, but.

Quick: The train has left the station.

Buffett: Yeah, exactly.

Quick: How come you don’t feel that way about shares of Apple? How come you feel like that’s a different story?

Buffett: Well, the shares, when we bought them at least, were much more reasonable in relation to current earnings. Apple didn’t have to do a lot better in the future than they were doing at the current time.

When you get into Google or Amazon you’re paying for the future more, but then they may well have a better future. I mean that may be more than justified, but, and Apple, I wouldn’t say it’s easier for me to understand than Google now perhaps or Amazon now but, it certainly would have been five years ago. It’s amazing where Apple’s ended up with consumers.

I mean, I can very easily determine the competitive position of Apple now and who’s trying to chase them and how easy it is to chase them. We happen to be well situated in terms of having these massive home furnishing stores and I can learn very easily how consumers react to different things. They’re probably easier than I can trying to pick out what’s really happening at Amazon at any given time.

Quick: So you use your research at the Nebraska Furniture Mart to tell you that consumers prefer Apple over Samsung, or I mean what type of thing are you…

Buffett: Well the interesting thing is if you come in to buy a TV set the furniture mart price is extremely important. Now obviously pictures, there’s all those great pictures just sitting up there, so you’re going to have Samsung you have all these different ones and if you put on a sale and you drop the price of samsung 10 percent, we can fill that department with people that come out for. You can’t move people by price in the smartphone market remotely like you can move them in appliances or all kinds of things.

I mean people want the product, they don’t want the cheapest product, and the loyalty is huge. Now that doesn’t mean somebody can’t come along with a product that just jumps the field in some way but, and then once you have the product the degree to which it sort of controls your life. I mean it’s a very very very valuable product to the people that build their lives around it. And that’s true of 8 year-olds and it’s true of 80 year olds.

Quick: People who have questioned Apple’s future have said things like, right now people are paying $800 for a smartphone and the other reality in technology is that prices eventually come down. And unless you’re adding more and more value to that product the price will come down so what happens if people, I mean I guess the question is will people always be willing to pay $800 or more for a phone, or will that wind up being a cost that comes down and down just as technology…

Buffett: Well it can be that way, but usually because there’s competition between different products and some manufacturer decides that they can’t beat say Apple on their own terms so they drop them 100 bucks or 200 bucks.

Some products are very susceptible to that and other products are not and so far, I mean you’ve had smartphones and big differences in price categories and people come back in, and if they had an Apple before you’re gonna have a much cheaper cell phone selling right next to a smartphone selling right next to it.

And they don’t look at it if you have a cheaper TV that picture’s looking at you, and you say, well i was like, what’s the difference, and you buy the cheaper TV and that’s true of, i mean, most items are price sensitive and it’s not to say that an Apple isn’t has somewhat price sensitivity. It’s very very very little, but somebody could come along and leapfrog something in the way of the technology and add some benefits that would be the more competitive threat to me than price competition, it would be benefit competition.

Quick: Yeah I don’t know what that is, but then you know Apple gave me a whole lot of things that i never realized…

Buffett: That’s the thing.

Quick: I needed until they came up with them.

Buffett: And somebody else was trying to think of some other things to give you along the same line.

Quick: Right. Let’s talk about just the stock price again you said that it made sense to you when you started buying into it. Shares have appreciated so…

Buffett: That’s the problem. I’m cheap, and there’s always an anchoring problem with buying stocks if you get used to buying them at x it’s harder to buy them at higher prices.

Quick: So does that signify that you’ve stopped buying in Apple because of where prices are?

Buffett: Well maybe, maybe not, but you slid it in there nice though.

Quick: Yeah I tried… I guess when you see things like the earnings that came out you had mentioned to us the other day that you weren’t bothered or disappointed by the earnings when you see…

Buffett: Not at all.

Quick: The stock price pull back, you probably like it at that point.

Buffett: Oh yeah, I mean Apple, with a non-new product, I think they sold something like 50 million, you know, that’s a lot of units to sell at $700 and a lot of those are going to people that are actually replacing a present Apple, but they do know that a new product is going to be out in six months or something and you know, who knows, maybe they got promised an Apple for their birthday or their graduation, but i would be tempted if i were going to buy one, to wait till a new model comes out. What do I lose by doing it, except the use of one in between? That’s a lot of product to sell with a new model coming out when you think about 50 million.